20

2014

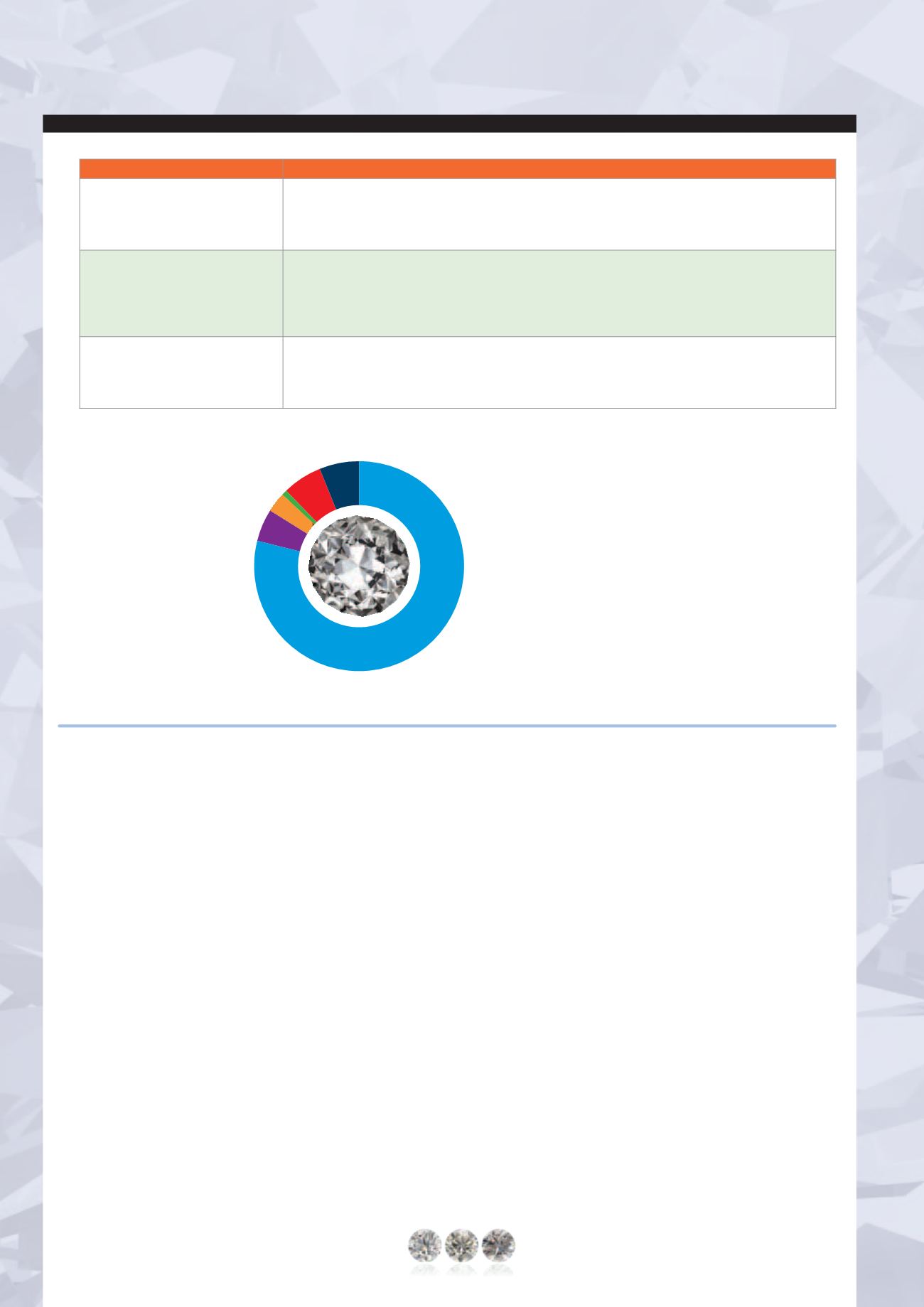

Revenue by

Geographic

Segment

Africa

5%

Europe

3%

India

79%

Note: India polishes approximately 90% of the world’s polished

diamonds (by stone count). It is natural that the majority of the Group’s

revenues are derived from India, given that we primarily supply high-tech

equipment and services to the rough diamond polishing industry to enable

production optimisation (speed and cost), risk minimisation and polished

yield maximisation, while revenues from other jurisdictions may increase

as we broaden commercialisation of new products and services catering to

the polished diamond trade (i.e., the Sarine Light™, Sarine Loupe™

and Sarine Profile™).

Israel

6%

North America

1%

Other

6%

RELATED ACTIVITY

TARGET CLIENT

Gross Profit

Gross profit for FY2014 increased by 13.4% to US$ 61.9 million, as compared to US$ 54.6 million for FY2013. For FY2014

the Group recorded a gross profit margin of 71% essentially the same as in FY2013. Gross profit included non-cash

amortisation expenses related to the amortisation of the Galatea know-how and previously capitalised Group research

and development costs of US$ 2.7 million and US$ 2.4 million, in FY2014 and FY2013, respectively.

Operational Profit

Profit from operations for FY2014 increased by 10.6% to a record US$ 32.9 million, as compared to US$ 29.8 million in

FY2013. For FY2014 the Group recorded an operating margin of 37.5% as compared to an operating margin of 39.0%

for FY2013.The decrease in our operating margin is due primarily to our increased expenses for research and development

and sales and marketing in line with our strategic investment in new products and services for the polished diamond trade

and non-diamond gemstones and their initial marketing efforts.

Net Profit

For FY2014 the Group reported a record net profit of US$ 27.2 million, an increase of 14.0% compared to net profit of

US$ 23.9 million for FY2013 (net profit before a one-time income tax expense for prior periods of US$ 26.5 million). For

FY2014, the Group recorded a net profit margin of 31.0% essentially the same as the net profit margin of 31.3% for

FY2013 (34.7% before the one-time income tax expense for prior periods).

Operating Review

Opportunities

Market-driven Opportunities

• Global economic indicators remain overall stable, with generally positive

developments in the U.S., still the largest single market for polished

diamonds, where diamond jewellery buying expanded marginally for

2014 and started 2015 with the best Valentine’s Day sales on record.

As the markets in Japan and Europe remain tepid the polished diamond

trade’s expectations are mostly focused on renewed demand from the

Chinese market, thus creating a more balanced demand in the global

diamond markets.

Company-driven Opportunities

• The Galaxy™ family of inclusion scanning products:

Deliveries of

Galaxy™ family (including Solaris™) systems in 2014 were a record 48

(46 in 2013 and 41 in 2012 and 34 in 2011). As of 31 December 2014

we had 190 systems deployed worldwide. Indeed, our recurring revenue

stream from the installed Galaxy™ and Solaris™ systems continues to

expand significantly, and accounted for most of the recurring revenue for

the year, which was over 35% of our overall revenues. We expect this

trend to continue in 2015. We continue to closely monitor our various

would-be competitors’ activities. The upgraded solution introduced by

our Russian competitor in 2014 has still not realised any commercial sales

(though some services are being offered), and promised improvements

have not been implemented. The system introduced by the Indian

competitor appears to have been aborted, as work on the prototype

systems has seemingly been abandoned. At a trade show in India in

December 2014 two new competitors indicated their intent to launch

competing systems, one Israeli and another Indian, but as of this writing

nothing tangible has materialised. Given our clearly superior integrative

solution with our extensive installed base of planning systems, the

Group expects to realise significant deliveries of Galaxy™ and Solaris™

systems in 2015, assuming positive industry sentiment. As we have now

successfully introduced systems covering stones from just under a carat

rough and up (the Solaris™, the Galaxy™ and the Galaxy™ XL), and

as we have also successfully addressed the need for high-resolution

scanning (the Galaxy™ Ultra), our research and development efforts

relating to our inclusion scanning family of systems is now turning to

the smaller stone sizes. The next stone range we are aiming to address

is 20 - 85 points rough, generally corresponding to polished stone sizes

of 7 – 20 points. As an indication of the potentially addressable market

at these stone sizes, it should be noted that 50 million polished stones

of 7 – 20 points are manufactured annually, fully fourfold the aggregate

numbers of all polished stones over 20 points in size, though it should

be remembered that there is not a one-to-one correlation between the

number of polished stones and that of rough stones.To achieve the return

on investment necessary for our customers to adopt the planned product,

our development focus will be on lowering the total cost of ownership

(TCO). Commercialisation is planned for late 2015 or 2016 having shown

promising initial results.

Sarine Technologies Ltd. • Annual Report

2014

Management’s Business Operations

& Financial Review