Half Year Financial Statement And Dividend Announcement 2025

Financials Archive

Condensed Consolidated Interim Statements of Profit or Loss and Other Comprehensive Income for the Six Months Ended 30 June 2025

Condensed Consolidated and Company Statements of Financial Position as at 30 June 2025

Review of Performance

Overview

The natural diamond manufacturing industry, from which the Group still derives most of its revenues, continues to

adjust to the “new norm” caused by the continued disruption of the market by lab-grown diamonds (LGD) offerings

and weak consumer demand in China. The LGD segment itself also continues to be affected by over-production and

oversupply driving declining wholesale and retail prices.

Notwithstanding challenging industry conditions which impaired our revenues in H1 2025 by 30%, as compared to

H1 2024, Sarine has made substantial progress in executing the strategic initiatives announced last year. The

aggressive business streamlining, coupled with the transitioning of the manufacturing activities to India have

mitigated, to a degree, the effect of the decline in revenues. The expansion of our Most Valuable Plan™ (MVP) for

optimising the planning of natural rough diamonds to additional stone sizes, the adaptation of our rough planning

technologies to LGD, and the opening of a GCAL by Sarine lab in India, have expanded our services portfolio,

attracted new customers and are generating new recurring revenue streams. These initiatives also bolster our

strategic position for value growth, when market conditions improve and are expected to foster long-term growth as

we expand our offerings for the natural stone and LGD markets alike.

In accordance with our strategy of recent years, the Group’s business continues to pivot to deriving mostly recurring

revenues from its proprietary services, including the Gal3D inclusion software (which processes the Galaxy®

platforms’ output) and Advisor® rough diamond planning cloud-based solution, along with other pay-per-use

services. Along with the Group’s grading and traceability reports, these now constitute most of the Group’s

revenues.

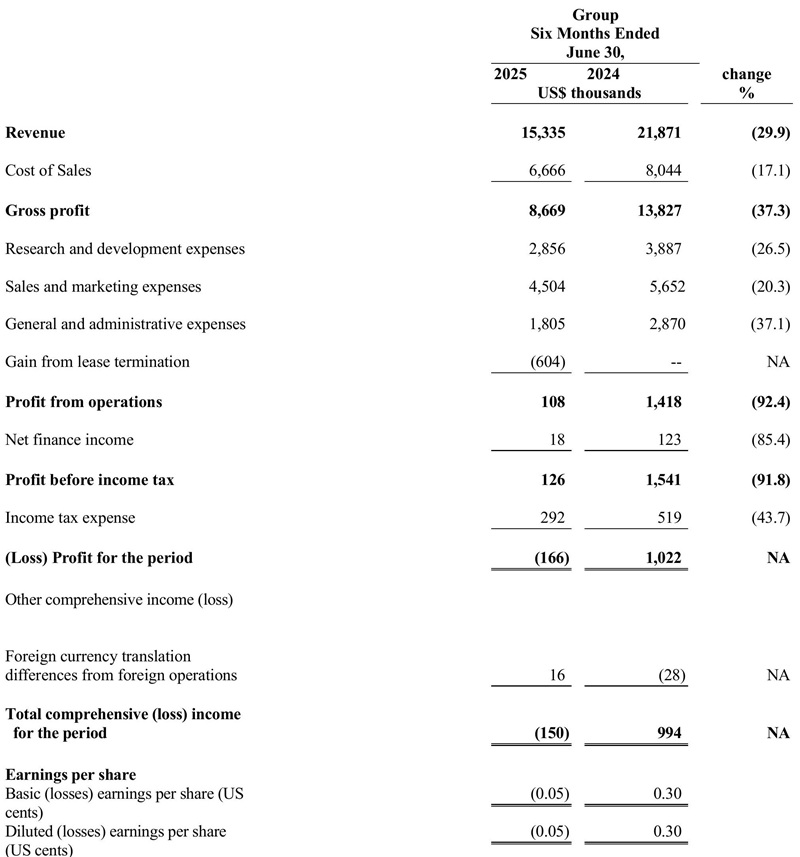

The Group reported revenues of US$ 15.3 million in H1 2025, minimal profit from operations of US$ 0.1 million,

and a net loss of US$ 0.2 million, as compared to revenues of US$ 21.9 million, profit from operations of US$ 1.4

million and a net profit of US$ 1.0 million in H1 2024. The Group EBITDA for H1 2025 amounted to US$ 1.6

million, as compared to EBITDA of US$ 3.3 million in H1 2024.

The decreased profitability for the six months ended June 30, 2025 compared to the six months ended June 30,

2024, was mainly due to lower sales and the lower gross profit margin, offset by the aforementioned cost reduction

steps implemented by the Group, the capitalisation of certain development costs relating to LGD grading

technology, due to the Group having achieved the required technological development benchmark, and the positive

impact of a lease termination.

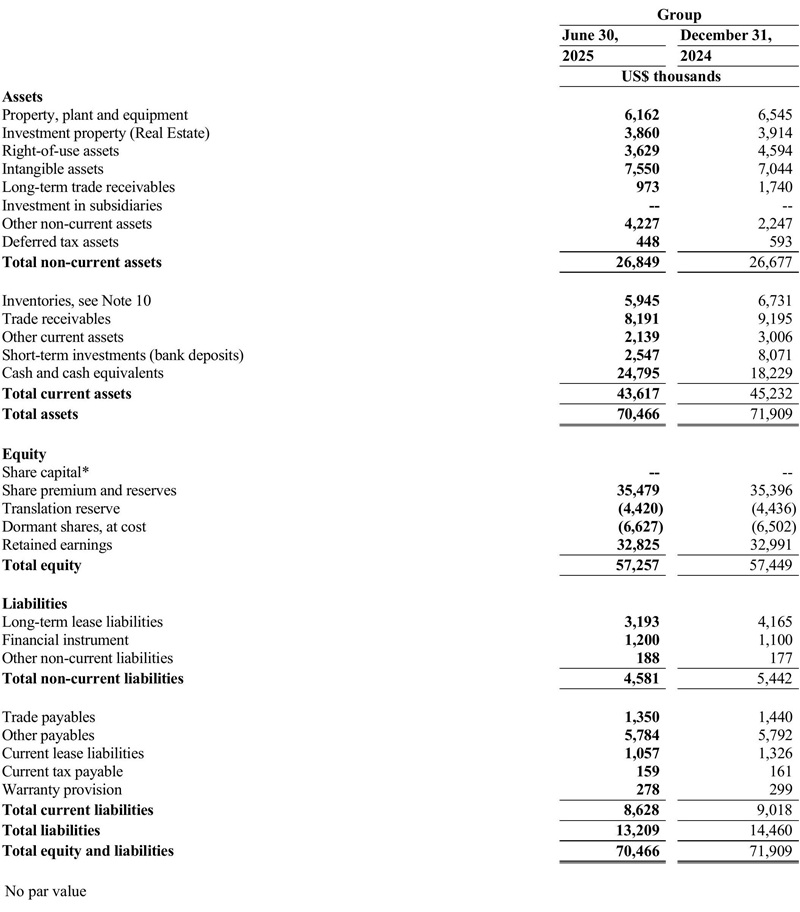

Balance Sheet and Cash Flow Highlights

As at June 30, 2025, cash, cash equivalents, short-term investments (bank deposits) (“Cash Balances”) increased to

US$ 27.3 million as compared to US$ 26.3 million as of December 31, 2024. The increase in Cash Balances was

primarily due to cash generated by operating activities, predominantly a decrease of trade and other receivables, to

US$ 11.3 million as at June 30, 2025 (US$13.9 million as at December 31, 2024), offset by tax deducted at source

payments which can be offset against future tax liabilities.

Revenues

Revenues for H1 2025 of US$ 15.3 million, decreased by 30%, as compared to revenues of US$ 21.9 million

reported in H1 2024. The decrease in revenues, was due to the continued decline in capital equipment sales coupled

with decline in recurring revenues due to lower quantities of rough natural diamonds entering the pipeline, a

reflection of the turbulent conditions affecting natural diamond industry.

Cost of sales and gross profit

Cost of sales for H1 2025 of US$ 6.6 million decreased by 17%, as compared to US$8.0 million reported in H1

2024 (on a decrease in revenues of 30%), with a gross profit margin of 57% in H1 2025 compared to 63% in H1

2024. The decrease in gross profit and the corresponding decrease in gross profit margin were primarily due to

decreased overall sales.

Research and development expenses

Due to the Group achieving the required technological development benchmark for capitalisation of some of its

LGD grading related development costs, a sum of US$0.7 million was capitalised in H1 2025. As a result Research

and development expenses for H1 2025 totalled US$ 2.9 million and decreased by 27% (16% including capitalised

expenses) as compared to US$ 3.9 million in H1 2024.

Sales and marketing expenses

Sales and marketing expenses for H1 2025 of US$4.5 million decreased by 20% as compared to US$ 5.7 million in

H1 2024. The decrease in sales and marketing expenses was due primarily to cost saving steps initiated by the

Group and fewer sales commissions.

General and administrative expenses

General and administrative expenses for H1 2025 of US$ 1.8 million decreased by 37%, as compared to US$ 2.9

million in H1 2024. The decrease in general and administrative expenses was primarily due to management

initiatives, mainly aimed at the reduction of IP-related legal costs, and the successful collection of debts previously

classified as doubtful.

Gain from lease termination

During H1 2025 the group terminated an office lease agreement in line with reduced staffing needs, prior to its

contractual termination date, resulting in a US$0.6 million cost savings windfall.

Profit from operations

The Group reported a profit from operations of US$ 0.1 million in H1 2025 compared to US$1.4 million in H1

2024. The decrease in in sales and in gross profit was offset by cost reductions and the windfall as detailed above.

Net finance income

Net finance income for H1 2025 was nil, as compared to US$ 0.1 million in H1 2024, mainly due to US$ 0.2

million exchange rate expenses.

Income tax expense

The Group recorded an income tax expense of US$ 0.3 million for H1 2025, as compared to US$ 0.5 million in H1

2024. The income tax expense was primarily due to the profitability being realised in various entities of the Group,

each subject to different jurisdictions, various applicable incentives, and income tax loss carryforwards.

Loss for the period

The Group reported a net loss of US$ 0.2 million in H1 2025 compared to a net profit of US$1.0 million in H1 2024

as cost saving steps, development capitalisation, and the windfall offset the lower gross profit, all as detailed above.

Commentary

We expect the following industry trends to continue influencing our business (also refer to section 6 above, the

Overview commentary):

-

Demand for natural diamonds is anticipated to overall remain stable at current levels as the new norm, due

to the LGD disruption of the retail diamond jewellery market, primarily, but not only, in the U.S. along with

the ongoing cutback in consumer spending in China. As the majority of diamonds are manufactured in

India, the impact of the recently declared U.S. tariffs of 50% on Indian exports to the U.S., has created

significant uncertainty in the market, and has initially caused major U.S. retailers to freeze deliveries from

India.

-

The LGD segment also faces challenges, as wholesale and retail prices continue to decline significantly,

posing problems both for manufacturers and retailers.

-

We continue our aggressive business streamlining and cost cutting, to meet the challenges of the current

market conditions. Our manufacturing activities have now been transferred to India, to take avail of our

qualified personnel in India to support our worldwide customers, maintaining our historic high-quality

standards, while benefitting from the substantially lower cost structure there.

-

The MVP adoption rate continues to improve, and its application continues to expand to additional sizes of

rough natural diamonds. The adoption is driven both by its creation of additional yield realised from the

rough material and its automation of the processes, generating cost savings. As our remuneration is based on

a per-stone fee, MVP generates new recurring revenues. With the ongoing expansion to larger sized stones,

as mentioned, we expect substantial growth of the MVP contribution in the next 12 months.

-

Our LGD-focused GCAL grading labs in Surat and New York offer a cost-effective venue with integrated

AI-based technology for our industry-unique guaranteed grading. We believe an opportunity for substantial

expansion of our grading business has been created by the GIA's recent announcement that they are

terminating the grading of LGD using the traditional 4Cs methodologies, as a means to differentiate LGD

from natural diamonds and reduce the cost of their grading services.

-

Environmental, social and governance (ESG) issues continue to concern retailers and luxury brands. Our

collaboration with DeBeers' Tracr™ platform, which went commercial in June 2025, along with our

AutoScan™ Plus and Sarine Diamond Journey™, provide a distinctively scalable cost-effective means to

meet any origin and traceability requirements, with minimal overhead or disruption to the diamond value

chain. We are witnessing increased interest from key U.S. retailers and expect to announce new adoption

during the second half of 2025.